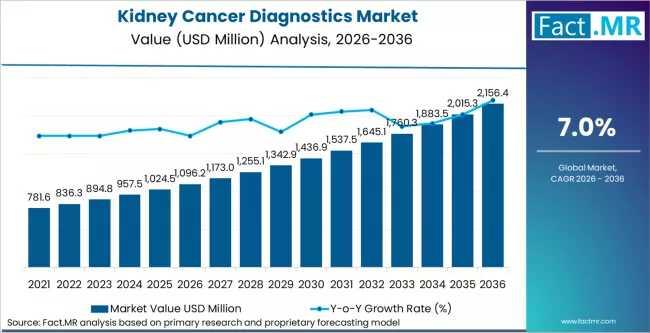

The global kidney cancer diagnostics market is poised for a decade of high-velocity expansion, with its valuation expected to climb from USD 1,096.22 million in 2026 to USD 2,156.42 million by 2036. According to the latest analysis by Fact.MR, the industry will advance at a steady compound annual growth rate (CAGR) of 7.0%. This growth is underpinned by a seismic shift in oncology toward precision diagnostics, where advanced imaging and liquid biopsies are redefining early detection and therapeutic monitoring for renal cell carcinoma (RCC).

Get Aceess Report Sample : https://www.factmr.com/connectus/sample?flag=S&rep_id=56

Kidney Cancer Diagnostics Market Quick Stats

- Market Size (2026): USD 1,096.22 Million.

- Projected Market Value (2036): USD 2,156.42 Million.

- Forecast CAGR:0% (2026–2036).

- Leading Modality: Imaging Diagnostics, accounting for 0% of modality revenue in 2026.

- Dominant Cancer Type: Renal Cell Carcinoma (RCC), representing 0% of market revenue.

- Key Growth Regions: Germany (7.4% CAGR), USA (7.1% CAGR), and Japan (6.8% CAGR).

- Top Companies: Hoffmann-La Roche AG, Siemens Healthineers AG, GE HealthCare Technologies Inc., Philips Healthcare, Thermo Fisher Scientific Inc., and Guardant Health Inc.

Market Momentum: The Shift Toward Molecular Precision

The trajectory of the kidney cancer diagnostics sector is intrinsically linked to the rise of personalized medicine. While traditional imaging modalities like CT and MRI remains the clinical cornerstone, the market is entering a "technology consolidation phase." Integrated platforms that combine AI-assisted image analysis with molecular data are increasingly favored by healthcare systems facing binary decisions between aging equipment and next-generation upgrades.

Vertical integration is becoming the preferred strategy for industry leaders. By controlling both the instrument platform and the consumable supply chain, companies are effectively mitigating the risks of diagnostic errors while maximizing margins through long-term service contracts.

Strategic Drivers of Growth

1. AI Integration and Workflow Automation

Leading OEMs are embedding AI-assisted decision support directly into imaging platforms. Innovations from GE HealthCare and Siemens Healthineers are reducing radiologist reporting time for incidentally detected kidney lesions, improving consistency in T-staging, and justifying premium pricing in hospital capital budgets.

2. Commercial Momentum in ctDNA and Liquid Biopsy

The FDA’s breakthrough designation for ctDNA-based kidney cancer recurrence monitoring is a game-changer. This allows for non-invasive post-surgical surveillance, generating repeat testing volumes that were previously unavailable through traditional biopsy methods.

3. Regulatory Catalysts (EU IVDR & FDA Modernization)

Regulatory compliance cycles are forcing a global equipment refresh. The mandatory transition to EU IVDR 2017/746 in Europe and 510(k) modernization in the US is compelling hospital networks to upgrade their renal oncology systems to satisfy new, stringent evidential standards.

Regional Outlook: Germany and USA Leading the Charge

| Country | Projected CAGR (2026–2036) | Key Market Influence |

| Germany | 7.4% | DKG-certified cancer center investment and IVDR compliance upgrades. |

| USA | 7.1% | CMS reimbursement expansion for ctDNA and FDA companion diagnostic approvals. |

| Japan | 6.8% | Precision oncology programs broadening molecular access for RCC staging. |

- North America: Remains the dominant force due to its robust R&D ecosystem and the presence of major diagnostic players like Illumina and Guardant Health.

- Europe: Germany is the regional engine, where government-funded programs are prioritizing technology refresh cycles in both primary and tertiary care settings.

- Asia-Pacific: Represents a massive greenfield opportunity. Expanding healthcare infrastructure and universal health coverage targets in India and China are funding first-time diagnostic procurement.

Segment Spotlight: Renal Cell Carcinoma (RCC) and Imaging

- Modality: Imaging Diagnostics hold over half the market share. The transition to digital pathology and AI-enhanced MRI is allowing radiology departments to handle increased throughput without proportional staffing increases.

- Cancer Type: RCC Diagnostics dominate because RCC represents roughly 90% of adult kidney cancers. The arrival of targeted therapies, such as Merck’s belzutifan, has created a mandatory requirement for genetic testing (VHL mutation analysis), further boosting market volume.

Competitive Analysis & Future Outlook

The market is moderately concentrated, with the top five firms holding up to 65% of global revenue. Strategic collaborations between diagnostic firms and pharmaceutical giants are essential for securing companion diagnostic (CDx) designations. For example, the link between Bristol Myers Squibb’s therapies and Roche’s PD-L1 assays has made immunohistochemistry volume a routine part of the RCC diagnostic workup.

Analyst Opinion:

"The Kidney Cancer Diagnostics market is moving past standalone devices. We are seeing a shift where integrated platforms with regulatory-validated performance data command the market. Suppliers who invest in digital health integration and outcome data analytics will be best positioned to sustain premium pricing through the next decade of contract renewal cycles." — Senior Analyst at Fact.MR

FAQ

What is the primary driver for the kidney cancer diagnostics market?

The rising global incidence of kidney cancer (over 431,000 new cases in 2022) combined with an aging population and technological breakthroughs in AI and molecular testing.

How is AI impacting the market?

AI tools are analyzing imaging scans and histopathological data with unprecedented speed, facilitating early detection and reducing diagnostic errors, which is critical for successful treatment outcomes.

Why is Germany showing the highest growth rate?

Germany’s growth is driven by strict adherence to the new EU IVDR regulations and significant investment in DKG-certified cancer centers, pushing for systemic diagnostic upgrades.

To View Related Reports:

Kidney Stone Management Devices Market https://www.factmr.com/report/1827/kidney-stone-management-devices-market

Kidney Dialysis Equipment and Supplies Market https://www.factmr.com/report/kidney-dialysis-equipment-and-supplies-market

Kidney Function Test Market https://www.factmr.com/report/kidney-function-test-market

Canine Kidney Supportive Care Products Market https://www.factmr.com/report/canine-kidney-supportive-care-products-market